Budgeting is more than a dry exercise in number crunching. It’s a plan that turns your goals into action, whether you run a household or manage a corporation. When you learn how a budget works, you gain control over your money.

This blog post breaks down what a budget is, why it matters and how to build one step by step. You’ll also see recent statistics that show how budgeting can reduce stress and improve financial wellbeing.

What is a Budget?

A budget is a forward‑looking plan for how you will earn and spend money over a set period. Governments, businesses and individuals create budgets to manage cash flows. The process starts by estimating income, such as sales revenue or wages, and then assigning that income to essential expenses, savings and other goals. Without a budget, it’s easy to let spending drift until you fall short when bills are due. With a budget, you have a map that tells your money where to go.

For example, a family might earn 1,200 Kuwaiti dinars per month. If they write down that rent costs 400 dinars, groceries cost 200 dinars and savings should be at least 100 dinars, they can see that discretionary spending should stay under 500 dinars. A budget turns vague wishes like “I should save more” into clear actions like “set aside 100 dinars on pay day.”

Why Budgeting Matters

Budgeting may feel tedious at first, but it has concrete benefits:

- Relieves stress. When you have a plan, you worry less about surprise bills. The Federal Reserve’s 2024 survey found that 55% of adults had emergency savings to cover three months of expenses, and those who always had money left over were far more likely to have savings. Knowing you’re covered for a rainy day frees your mind for other goals.

- Prevents debt. A 2025 Debt.com survey showed that more than 86% of people say they budget regularly and that over 84% report budgeting helps them avoid debt or pay it off. When you track spending, you catch overspending before it turns into high‑interest debt.

- Saves time and boosts productivity. Vanguard research found that investors without emergency savings spend 7.3 hours per week thinking about their finances, compared with 3.7 hours for those with at least $2,000 in savings. Workers without savings also spent four times as many hours distracted by financial stress at work. Budgeting and saving free up mental bandwidth.

- Supports growth. With a clear budget, organizations can plan for future investments, decide when to expand and avoid wasteful spending. Individuals can save for education, home ownership or retirement.

- Meets legal requirements. Many public companies must produce budgets and financial reports for shareholders and regulators.

Types of Budgets

Budgeting is not one‑size‑fits‑all. Different situations call for different approaches. Below are several common categories and methods.

Corporate Budgets

Businesses rely on budgets to allocate resources and plan ahead. Common corporate budgets include:

- Operating budget. This plan covers day‑to‑day expenses like salaries, rent and utilities. It forecasts expected sales and matches spending to projected revenue. For example, a retail chain might forecast sales of KWD 500,000 for the quarter and cap payroll and inventory expenses at KWD 450,000 to preserve a profit margin.

- Capital budget. Companies use capital budgets to plan long‑term investments in equipment, property or technology. An oil firm considering a new refinery would outline the project’s expected cost, timeline and return on investment. Careful capital budgeting helps avoid overspending on projects that don’t add value.

- Cash‑flow budget. Even a profitable business can run out of cash if revenues arrive after bills are due. A cash‑flow budget tracks the timing of cash inflows and outflows so the company can arrange financing or adjust payment schedules.

- Master budget. Large organizations create a master budget that combines operating, capital and cash‑flow budgets. It provides a comprehensive view of all departments and ensures every unit aligns with overall strategy.

Individual Budgets

Personal budgets range from simple to highly structured. Choose the one that fits your habits and goals:

- Envelope budget. You assign money to different categories, rent, groceries, transport, and put cash or the equivalent amount in separate envelopes or digital wallets. When an envelope is empty, you stop spending in that category until the next pay period. This hands‑on method helps prevent impulse purchases and is ideal for people who like tactile reminders.

- 50/30/20 plan. This rule divides income into 50% for needs (housing, food, transport), 30% for wants (dining out, entertainment) and 20% for savings and debt repayment. If you earn 1,000 dinars, allocate 500 to essentials, 300 to discretionary spending and 200 to savings and debt.

- Zero‑based budget. Every dinar is assigned a job, leaving zero unallocated. You list your income and plan expenses, rent, food, savings, donations, until your budget equals your income. This method offers tight control and ensures no money drifts away unnoticed.

- Pay yourself first. You commit to saving a set amount or percentage as soon as you receive income. The remaining amount covers living expenses. Automated transfers make this method easy and help build savings without feeling the pinch.

- No budget. Some people prefer a flexible plan: they pay necessary bills and save a target amount, then spend the rest freely. While simple, this approach requires discipline to avoid overspending.

Outcome‑Based Budgets

Budgets can also be classified by the relationship between revenue and spending:

- Surplus budget. Revenues exceed expenses. Governments or households may deliberately aim for a surplus to pay down debt or build reserves.

- Balanced budget. Revenues equal expenses. Many public agencies target a balanced budget to show fiscal responsibility.

- Deficit budget. Expenses exceed revenues. Temporary deficits may be acceptable for investments or emergencies, but chronic deficits can lead to unsustainable debt.

Static Vs Flexible Budgets

- Static budget. A static budget sets fixed spending limits for each category and doesn’t change during the budget period. Small businesses often use static budgets when costs are predictable. The advantage is clear limits; the disadvantage is that it may not adjust to unexpected changes.

- Flexible budget. This budget adjusts spending limits based on changes in revenue or activity. For example, a manufacturing firm might allow its materials budget to rise if sales exceed forecasts. Flexible budgets offer adaptability but require more monitoring.

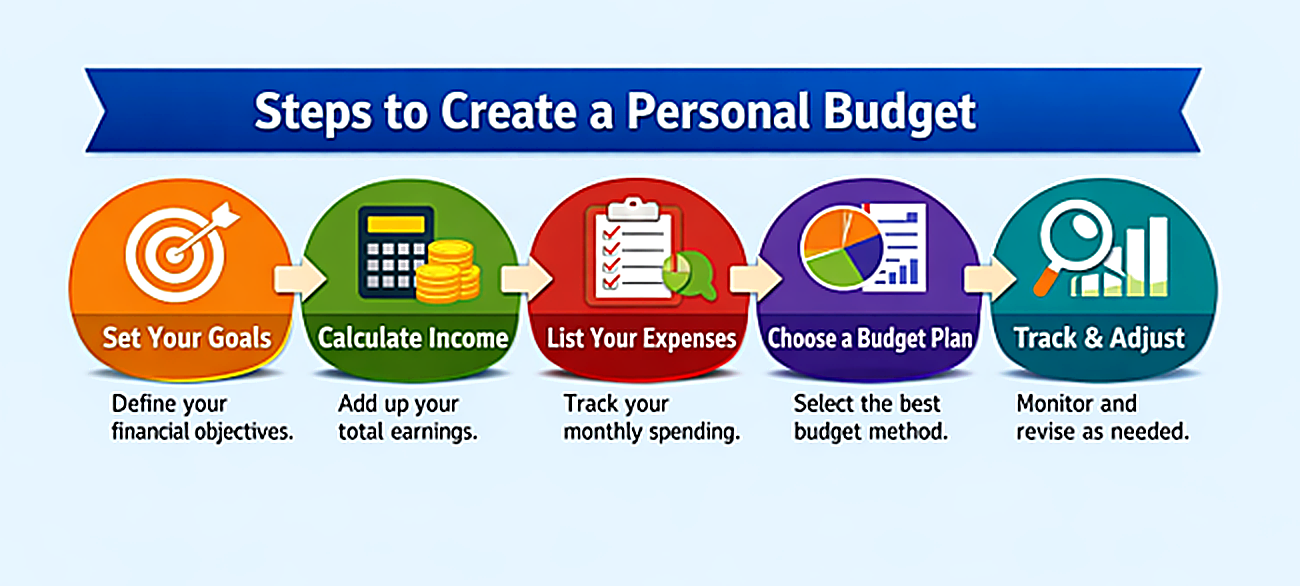

How to Create a Personal Budget

Building a budget can feel daunting, but breaking it into clear steps makes it manageable. Follow the process below and refer to the infographic for a visual guide.

- Define your goals. Decide what you want your budget to achieve. Do you need to pay off debt, build an emergency fund, save for a vacation or all three? Clear goals guide your decisions.

- Calculate your income. List all sources of income after taxes, salary, freelance work, interest, or support payments. Use the net amount you actually take home.

- List your expenses. Track every expense for a month. Include fixed costs (rent, utilities, loan payments) and variable costs (food, transport, entertainment). Don’t forget occasional expenses like gifts or medical bills.

- Choose a budget type. Based on your habits and goals, choose one of the methods above. If you prefer simplicity, the 50/30/20 plan may work. If you like precision, consider a zero‑based budget.

- Review and adjust. A budget is a living document. Track your actual spending and compare it to your plan. Adjust categories or choose a different method if needed. Celebrate small victories, like paying off a credit card or meeting your savings goal.

Purpose of Budgeting

Budgeting serves several purposes beyond daily money management:

- Planning and coordination. Organizations use budgets to align departments and schedule activities. For example, the marketing department cannot schedule a campaign without knowing the available funds, and production teams need to know equipment budgets to plan manufacturing.

- Control and accountability. Budgets set limits and performance targets. Managers compare actual spending against the budget to identify variances. If a cost overruns, they investigate why and adjust.

- Communication. A written budget communicates priorities to stakeholders, employees, investors and lenders. It shows where resources are going and why.

- Motivation. When people participate in creating a budget, they feel a sense of ownership. Achieving budgeted goals can be motivating, whether it’s staying under a travel allowance or hitting a sales target.

- Regulation and reporting. Many governments require budgets by law. Public companies must disclose financial plans in annual reports to maintain transparency with shareholders.

Tips for Effective Budgeting

Creating a budget is just the starting point. The following tips can help you stick with your plan and maximize results:

- Track your spending regularly. Use a notebook, spreadsheet or mobile app to record expenses. Review the totals weekly to see if you’re staying on track.

- Automate savings. Set up automatic transfers to savings accounts or investments on payday. When saving happens before spending, you are less tempted to skip it.

- Build an emergency fund. Aim to save at least the equivalent of one month’s expenses, then grow toward three to six months. Vanguard research shows that even $2,000 in savings is linked to higher financial well‑being.

- Review your budget each month. Circumstances change, prices rise, income fluctuates, and goals evolve. Adjust your budget to reflect reality. Celebrate progress rather than focusing on missteps.

- Use tools and support. Budgeting apps like Mint, YNAB or simple spreadsheets can simplify tracking. Some people benefit from accountability partners or financial coaching.

- Link budgeting to goals. Instead of viewing budgeting as deprivation, think of it as a tool for reaching goals, buying a home, traveling the world or starting a business. Connecting daily choices to future dreams makes budgeting meaningful.

FAQs

Q1. What is the best budgeting method?

The best method is the one you’ll use. If you like structure, try zero‑based budgeting. For simplicity, the 50/30/20 plan works well. Test different methods and see which feels right for you.

Q2. How much should I save in an emergency fund?

Experts suggest starting with $2,000 or about half a month’s expenses. Over time, build toward three to six months of living costs. The goal is to handle unexpected expenses or a temporary loss of income.

Q3. Can a budget help me pay off debt faster?

Yes. By tracking income and expenses, a budget shows how much you can allocate toward debt. Debt.com’s survey found that 84% of budgeters say it helps them avoid or pay off debt.

Q4. How often should I review my budget?

Review your budget at least once a month. Check that your spending matches your plan, adjust categories and update income or expense changes. Regular reviews keep your budget realistic.

Q5. Is budgeting only for people with steady incomes?

No. Freelancers and gig workers benefit from budgeting, too. Estimate your average monthly income, prioritize essential costs and save more during high‑earning months to cover lean periods. A flexible budget can adapt as your income fluctuates.

Conclusion

A budget gives you a clear view of your money and helps you make better choices every day. It shows where your income goes and highlights areas you can improve. With a simple budget, you can control spending, reduce money stress, and plan for future needs. Budgeting works for individuals and organizations alike. When you review and adjust your budget often, it stays useful and realistic. Over time, this habit builds confidence and supports steady financial progress.