Consumer surplus is one of the most important ideas in microeconomics. It explains the extra value buyers receive when they pay less than what they are willing to pay. In simple terms, consumer surplus shows the benefit consumers gain in a market.

This concept helps us understand how prices, demand, and satisfaction connect. Businesses use it to set pricing strategies, and governments use it to measure economic welfare.

In this blog post, you will learn the meaning of consumer surplus, its formula, graph explanation, and real-world examples that show why it matters in today’s economy.

What is Consumer Surplus?

Economists define consumer surplus as the extra value that buyers receive when they pay less than the highest price they are willing to pay. A consumer surplus is the gap between your maximum price and what it costs in the market. Imagine you planned to spend $800 on a smartphone but found a promotion at $500; the $300 difference is your surplus. In simple terms, consumer surplus measures the benefit you enjoy from a purchase beyond the monetary cost.

Consumer surplus arises because of marginal utility, the added satisfaction gained from each additional unit of a good or service. As people consume more units, the pleasure from each extra unit declines. This downward‑sloping satisfaction curve helps explain why demand curves slope downward and why consumer surplus exists.

History and Theory

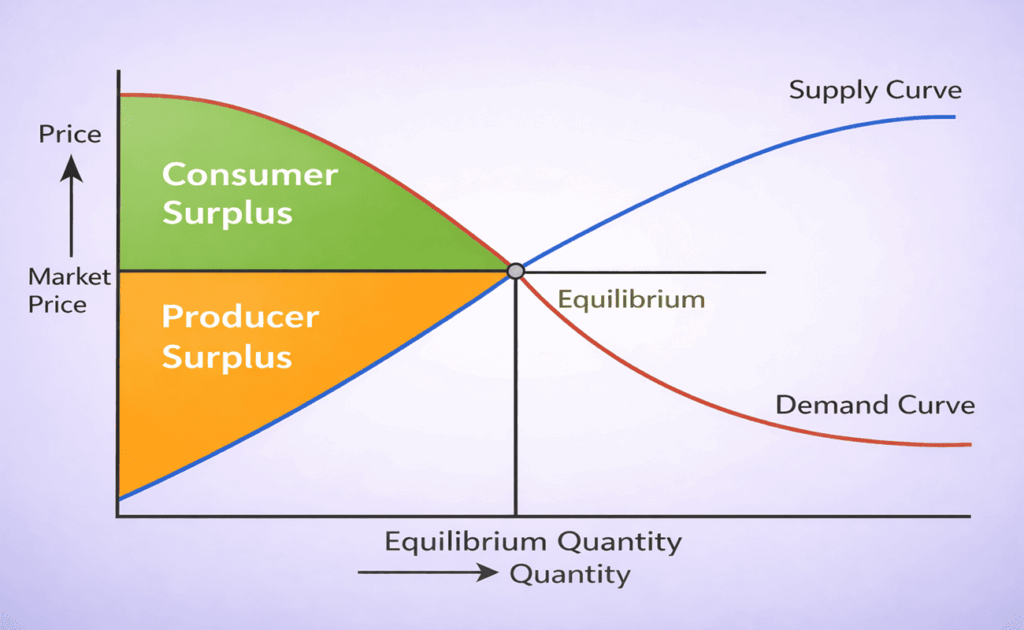

The idea of measuring consumer surplus dates back to the 1840s. French engineer Jules Dupuit used it to evaluate the benefits of public works such as bridges and canals. Later, economist Alfred Marshall formalized the concept in his 1890 book, Principles of Economics. Marshall demonstrated how consumer surplus appears as the triangular area under the demand curve and above the market price line. Since then, consumer surplus has become a key tool for understanding welfare economics, tax policy and market efficiency.

Formula and Graphical Representation

Economists calculate consumer surplus using a simple formula:

where Qd is the quantity at equilibrium and △P is the difference between the maximum price consumers are willing to pay and the equilibrium price. For example, if consumers would pay up to $100 for a product but can buy it for $70, and 1,000 units are sold, the surplus is 1⁄2×1,000×(100-70)=$15,000.

Graphically, consumer surplus appears as a triangle on a supply‑and‑demand chart. The downward‑sloping demand curve reflects consumers’ willingness to pay at various quantities, while the horizontal line shows the market price. The green area in the chart below represents the surplus enjoyed by consumers when the price is lower than what they would have paid.

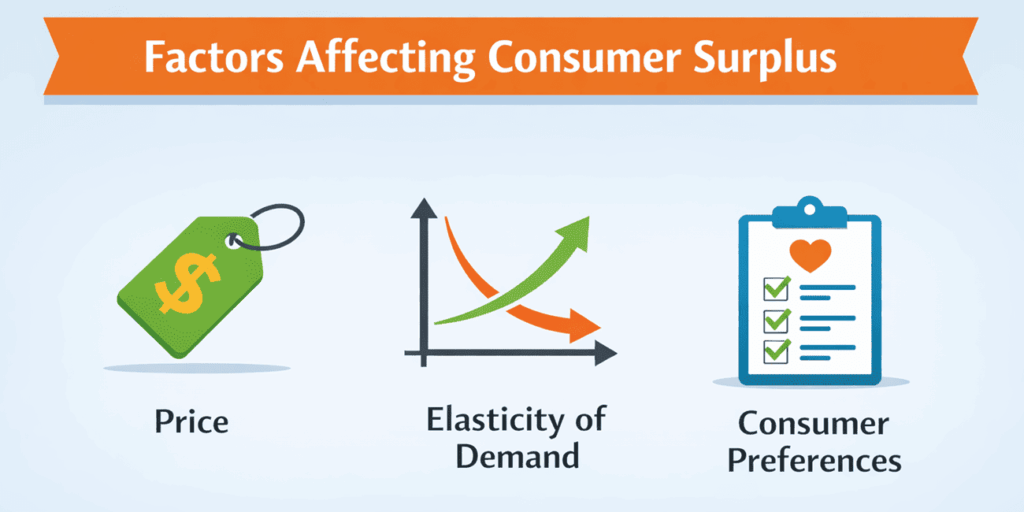

Factors That Influence Consumer Surplus

Multiple factors determine the size of consumer surplus:

- Prices: Lower prices widen the gap between willingness to pay and actual price, increasing surplus. Higher prices shrink the gap.

- Elasticity of Demand: When demand is inelastic, consumers continue buying even as price increases, creating high surplus. When demand is elastic, a small price change greatly alters demand and surplus drops.

- Consumer Preferences: Preferences, income and awareness shape how much satisfaction a buyer derives from a product. Changes in tastes or trends can shift the demand curve and alter the surplus.

The illustration below summarizes these factors.

Consumer Surplus in Digital and Free Markets

Consumer surplus is especially visible in digital markets and when goods or services are offered for free. A 2025 essay from the Federal Reserve Bank of St. Louis notes that “consumer surplus … is maximized” when an item is free. When the price is zero, buyers capture the full value of the product, and the triangular area of surplus effectively covers the entire demand curve. Think about the value you receive from services like email or search engines; even though you pay nothing, the benefit is immense.

Free shipping offers a similar effect. The same Federal Reserve article explains that up to 48 percent of online shoppers abandon their carts when shipping charges appear. Retailers often encourage consumers to spend a bit more to qualify for free shipping because buyers perceive greater value in adding another item rather than paying for delivery. Offering free shipping enlarges the consumer surplus by reducing the perceived cost, thereby increasing demand and transaction value.

Real‑World Examples

Smartphone Deal. You’re willing to pay $800 for a latest‑model smartphone, but a sale drops the price to $500. Your consumer surplus is $300. That extra value may be spent on accessories or saved for future purchases.

Airline Tickets. Airlines use dynamic pricing to capture some of the consumer surplus. When you buy a ticket months in advance for $300 but would have paid up to $500 for a peak‑season flight, you enjoy $200 in surplus. Around holidays, carriers raise prices, shifting part of the surplus to producer surplus.

Gasoline. Suppose gas costs $5 per gallon in the city but $4 per gallon out of town. If you’re willing to pay up to $5, your surplus per gallon at the cheaper station is $1. Over a 15‑gallon fill‑up, that’s $15 in savings.

Streaming Service. A streaming subscription costs $10 per month. If your enjoyment of the content is worth $20 to you, each month you experience $10 in surplus. This motivates many companies to introduce premium tiers to capture some of that extra value.

These examples show that consumer surplus is both tangible and everyday. Recognizing where it exists can help you make better purchasing decisions.

Consumer Surplus Vs Producer Surplus

While consumer surplus measures the benefit to buyers, producer surplus measures the benefit to sellers. Producer surplus is the difference between the minimum price producers would accept and the actual price they receive. On a supply‑and‑demand graph, producer surplus sits above the supply curve and below the market price line. Together, consumer and producer surplus make up economic welfare or total surplus.

In perfectly competitive markets, both surpluses are maximized; in monopolistic markets, producers often capture more of the potential consumer surplus by charging higher prices.

Criticisms and Limitations

Consumer surplus is a useful tool, but it relies on several assumptions:

- Measurable Utility. The concept assumes that utility can be measured and compared across consumers, yet satisfaction is subjective.

- Ceteris Paribus. It assumes tastes, income and other factors remain constant.

- No Substitutes. The theory presumes that substitutes are limited or absent. In reality, many markets have substitutes that alter willingness to pay.

- Constant Marginal Utility of Money. It assumes that the value of money is constant for consumers. This may not hold when incomes change.

These limitations mean that consumer surplus is an approximation. It provides a useful framework for analyzing welfare but should be interpreted carefully alongside qualitative insights.

FAQs

Q1. What is consumer surplus in simple terms?

Consumer surplus is the difference between the highest price you would pay for something and the actual price you pay. It shows the extra value you get from a good or service.

Q2. How do I calculate consumer surplus?

First, draw the demand curve and find the market price. Then use the formula 1/2 x Qd x △P to compute the area of the surplus triangle.

Q3. Why does consumer surplus matter?

It helps economists and policymakers evaluate how price changes, taxes or regulations affect consumer welfare. A larger surplus means buyers enjoy greater benefit from purchases.

Q4. What factors decrease consumer surplus?

Higher prices, elastic demand and changes in preferences or income can shrink the surplus. Monopoly pricing can also shift surplus from consumers to producers.

Q5. Does free shipping increase consumer surplus?

Yes. Research shows that when shoppers see shipping charges, up to 48 percent abandon their carts. Free shipping reduces the effective price, increasing the surplus and encouraging purchases.

Summary

Consumer surplus shows the extra benefit buyers receive when they pay less than what they are willing to pay. It helps explain how markets create value for consumers. By using the consumer surplus formula and graph, you can see how price changes affect demand and overall welfare. Businesses, economists, and governments use consumer surplus to guide pricing, policy, and strategy decisions. Understanding this concept gives you a clearer view of how markets truly work.