Controlling is a key management function that ensures work is done efficiently and organizational goals are achieved. It helps managers oversee their subordinates, give clear commands, and maintain discipline. By monitoring activities, controlling ensures that organizational resources are used effectively, minimizing waste and maximizing productivity.

This function operates at all levels, from top management to lower levels in organizations and projects. Through control, managers align ongoing activities with the planned objectives, ensuring progress stays on track.

Controlling is closely linked to planning, yet they are distinct processes. Planning is forward-looking, formulating goals, and defining a course of action to achieve them. In contrast, controlling is backward-looking, as it assesses actual performance, compares it against the plan, and provides feedback to address gaps.

Organizations can operate smoothly by combining control with other management functions, developing accountability, and driving long-term success.

How Controlling Functions Are Helpful

Controlling functions plays a crucial role in ensuring an organization runs smoothly. These functions are needed at all levels of management, from top executives to team leaders. They help managers pass on instructions from top management, assign tasks to their subordinates, and ensure the work is completed on time.

Through controlling, managers can monitor performance and check if the organization’s activities align with the goals. This helps identify problems early and adjust to keep everything on track. Controlling also ensures that resources like time, money, and manpower are used efficiently, minimizing waste and increasing productivity.

Controlling creates a structured environment where employees understand their responsibilities by maintaining discipline and providing clear instructions. Feedback collected during control helps managers improve workflows, make better decisions, and refine plans.

Controlling functions ensure accountability, enhance coordination, and help the organization achieve its objectives effectively and efficiently.

Types of Controlling

Controlling can be of the following types

1. Feedback Control

Feedback control allows managers to review past performance and identify areas for improvement. They use this information to make necessary process adjustments, reducing errors and discrepancies. It also helps managers incorporate new features based on customer requests and feedback. This type of control is often referred to as post-action control.

2. Concurrent Control

Concurrent control focuses on real-time monitoring of activities as they happen. Managers observe work progress, check for compliance, and take immediate corrective action if needed. This dynamic approach ensures problems are addressed promptly before they escalate. Concurrent control is crucial for maintaining quality and meeting deadlines.

3. Feedforward Control

Feedforward control involves identifying potential problems before they occur and taking proactive measures to prevent them. Managers communicate expectations and guide to mitigate risks. This type of control is also known as predictive control. While it can sometimes require significant process changes, it ensures the organization stays prepared and minimizes future deviations.

4. Behavioral Control

Behavioral control evaluates the performance of employees, managers, and departments. Using tools like balanced scorecards, management reviews achievements, updates targets, and rewards top performers. This type of control ensures accountability and motivates employees to strive for better results.

5. Monetary Control

Monetary control involves managing both financial and non-financial resources effectively. Managers focus on budgets, monitor expenses, and evaluate the return on investment (ROI). Organizations can maintain financial discipline and achieve strategic goals by assigning department budgets and tracking their performance.

Importance of Controlling

Controlling is important for the following reasons:

1. It Creates Discipline in Employees

Controlling ensures that employees follow the rules and perform their tasks responsibly. When there is proper monitoring, employees stay on track and avoid actions against organizational policies. It motivates employees to meet performance standards and avoid mistakes. Consistent control creates a sense of accountability, making the work environment more professional and focused.

2. It Helps Managers Get Work Done

Managers use controlling to check whether tasks are completed as planned. It allows them to identify delays or mistakes and take corrective actions. Regular control keeps employees aware of deadlines and encourages productivity. It also helps managers maintain a clear view of team progress, ensuring everyone contributes to achieving goals.

3. It Establishes Authority and Chain of Command

Controlling reinforces the structure of authority within the organization. Employees understand who they report to and what is expected of them. It ensures that everyone respects the reporting structure, making it easier to manage teams. Additionally, it prevents misunderstandings by providing clear guidelines on responsibilities and decision-making.

4. It Helps Efficient Use of Resources

By monitoring activities, controlling prevents waste of resources like time, money, and materials. It ensures that everything is used effectively to achieve the best possible results. Controlling helps identify areas of improvement in resource allocation. This allows the organization to optimize costs and improve overall efficiency.

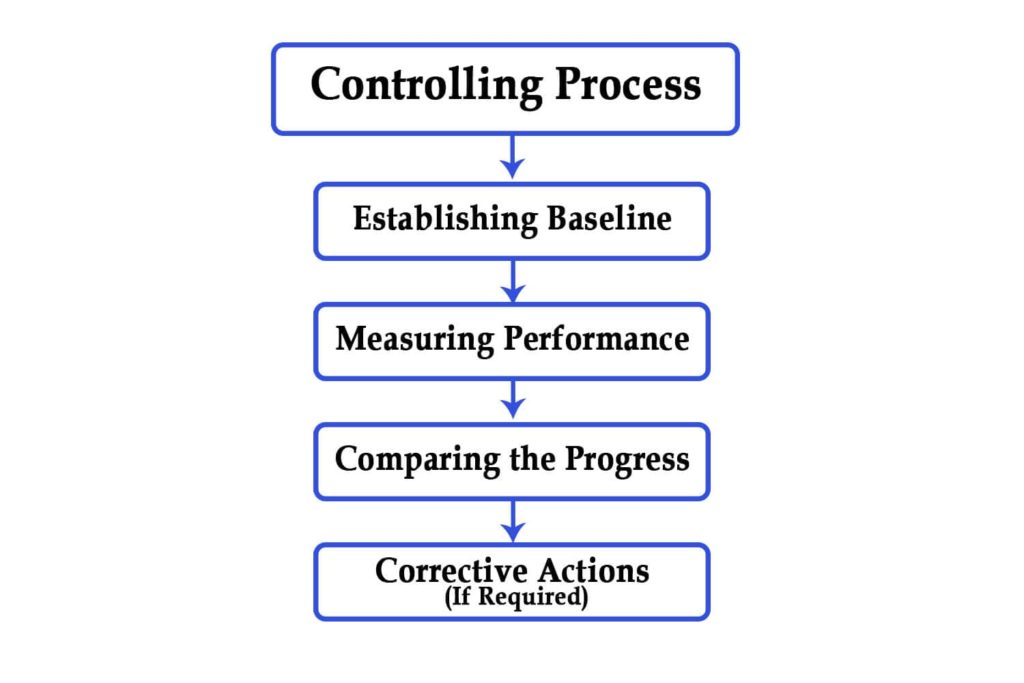

Steps of the Controlling Process

Controlling requires the following steps:

Step 1. Establishing Baselines

The first step in the controlling process is to set baselines or standards for performance. These are specific goals or benchmarks that the organization aims to achieve. Baselines provide a clear reference point for tracking progress. Without defined standards, measuring success or identifying gaps would be impossible.

Step 2. Measuring Performance

Once baselines are established, the organization collects data to measure actual performance. This includes recording outputs, reviewing reports, and assessing key metrics. Accurate performance measurement is essential for identifying whether the organization meets its standards.

Step 3. Comparing the Progress

At this stage, managers compare the recorded performance with the baselines. This comparison highlights gaps, deviations, or achievements. It helps determine if the organization is on track or if issues need attention. A systematic comparison makes it easier to pinpoint the source of any problems.

Step 4. Taking Corrective Action

If the actual performance matches the baselines, no further action is necessary, and the organization can continue its operations as planned. However, corrective action is required if performance deviates from the set standards. Managers identify the causes of deviations and implement changes to align performance with goals. This may involve adjusting processes, reallocating resources, or addressing inefficiencies.

Summary

Controlling is a vital process that bridges the gap between planned and actual performance in any organization. By monitoring activities, measuring progress, and comparing results with set standards, controlling helps ensure that tasks are completed on time, within budget, and with the desired quality. It enables managers to identify deviations, take corrective actions, and maintain efficiency in operations.

Controlling creates discipline, accountability, and the optimal use of resources, driving overall organizational success. An effective controlling process ensures that goals are achieved and continuous improvement is prioritized, creating a strong foundation for growth and stability.