A market structure includes buyers and sellers and the forces of demand and supply.

Market structures can be purely competitive. For example, businesses can have a perfect system of buyers and sellers, monopolistic (one seller and many buyers), duopolistic (two sellers and many buyers), or oligopolistic (few sellers and many buyers) markets.

A company has a monopoly if it is a profit maximizer, price maker, single seller, and practicing price discrimination in a market with a high barrier to entry. Proponents of monopolies believe that monopolies are largely concerned with efficiencies of scale in production.

However, many experts counter this claim because the monopoly can exploit the consumer by restricting production and variety or charging higher prices due to its ultimate power.

What is a Monopoly?

Definition: A monopoly is a single firm controlling price and market with no existing competitor. A monopolist is a price maker and can set the amount of the product it sells.

In simple words, when one business controls the market or a sizeable percentage of the market, the business has a monopoly.

According to Irving Fisher, a renowned American neoclassical economist, a monopoly is a market in which there is the “absence of competition,” creating a situation where a specific person or company is the only supplier of a particular good/service.

Government can establish it; it can form naturally or by integration. A monopoly is a market structure in which a single supplier produces and sells a given product or service.

The online Britannica conceptualizes a monopoly implies an exclusive market possession by a product or service supplier for which there is no substitute. The supplier determines the product’s price without fear of competition from other sources or through substitute products.

In law, a monopoly is a business entity with significant market power, that is, the power to charge excessively high prices. A single entity controls a particular industry in the purest form of a monopoly. Many experts consider controlling 25% of the market share a monopoly.

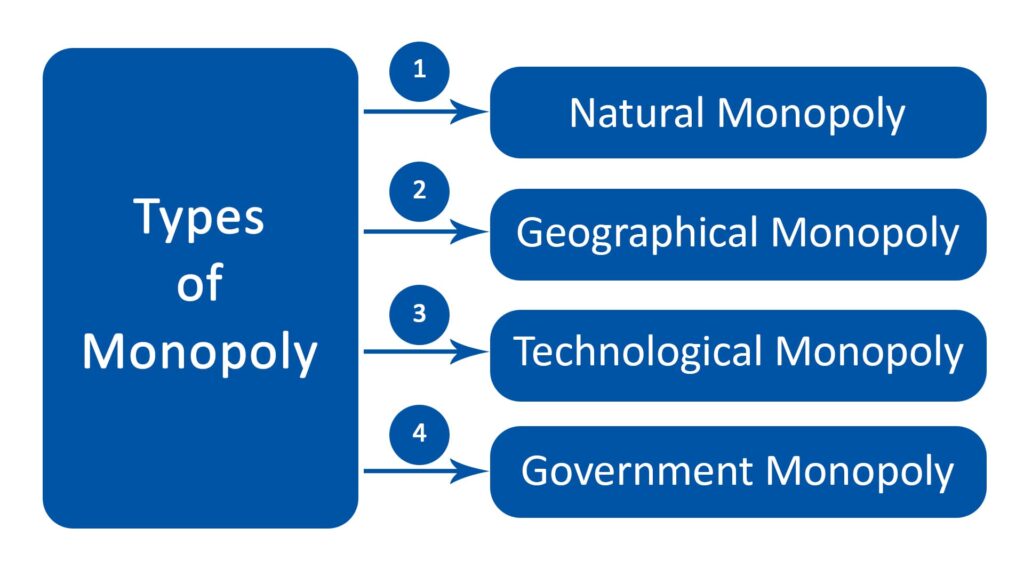

Types of Monopoly

Monopoly can exist in the following forms:

Natural Monopoly: This market is characterized by high start-up costs and, thus, the most efficient for one business to offer a product or service. Refineries in most developing countries are state-owned due to the high initial investment capital involvement. Therefore, it could be the case of the first seller in a capital-intensive market.

Geographic Monopoly: One business provides a service/product to one area. No competitor wants to enter the market, perhaps because of the remoteness of the location or low-profit margin. Hence, a single seller enjoys the region.

Technological Monopoly: This is based on a process or product’s proprietary or intellectual property right. The technology owners only have the right to sell the product. For instance, Universal Oil Products (UOP) reserves a technology monopoly on various industrial processes, e.g., Linear Alkyl Benzene production. A competitor only comes into the market if they can develop a substitute process.

Government Monopoly: This is a government-imposed market; most times, it is for regulatory reasons. For example, the government may control electricity supply and distribution for strategic reasons.

Characteristics of a Monopoly

The following characteristics can identify monopolies:

- Lack of Competition: A regional airport serving a single airline.

- Lack of Substitutes: The product or service enjoys unparallel uniqueness within the market.

- Price Changes Without Recourse: A monopolist effectively sets the price. Because no competing products offer a different price, the monopolist effectively sets the rate for the entire industry.

- Entry Barriers for Competitors: A combination of government regulations, pre-existing contracts, and insurmountable price factors make it impossible for a competitor to enter the market. Many municipal cable TV operators benefit from massive barriers to entry for potential competitors. It is difficult to break a monopoly without new entrants into a market.

It is important to note that monopolies derive their market power from barriers to entry – circumstances that prevent or greatly impede a potential competitor’s ability to compete. The barriers can be economic, legal, or deliberate.

Arguments For and Against Monopoly

Monopolies are considered negative for all parties except for the company owners. However, sometimes it positively affects consumers in a monopolistic marketplace. These include:

Price Stability: In the absence of competition, there are no price wars to rattle markets. Other companies and end-user customers who do business with monopolistic companies enjoy price certainty.

Economies of Scale: A company with a monopoly on a product can produce mass quantities at lower costs per unit. They can pass those low prices along to the consumers.

Research and development (R&D) Budget: A monopoly that feels confident about its market standing feels safe investing in R&D. This leads to new products and manufacturing efficiencies that will benefit consumers. The pharmaceutical industry offers an example of this.

The arguments against monopoly are for the following reasons:

Increased Prices: When a single firm controls the industry, prices typically rise. Airports served by a single airline face the negative price consequences of a single seller’s market power. Generally, the closer to a pure monopoly within an industry, the higher the average consumer price of goods and services.

Inferior Products: Monopolistic firms have minimal incentive to improve product and service quality. For example, if consumers are dissatisfied with a monopolistic cable company, they may have little choice apart from stop watching TV.

Price Discrimination: A monopolistic company can easily discriminate, charging different prices for consumers. For example, in a sports stadium, spectators pay a different fee for a hot dog, depending on their seating arrangements.

Control and Regulation of Monopoly

The authority places control and regulation mechanisms to check excessive profit by the monopolists, which eventually impacts the buyers. These are:

Anti-Monopoly Laws: Here, the government enacts legislation restricting trade practices that can result in a company controlling a large market share. They could also impose laws that restrict mergers to avoid market domination.

Price Control Agencies: Government can set up a unit or commission to fix the price for the monopoly product below the monopoly price, thereby increasing output and lowering the cost for the consumer.

Taxation: The authority may impose a tax to discourage monopoly.

Summary

In a monopoly, a single firm or organization controls the price and market. It benefits company owners as they can raise prices and reduce services without consequence. However, they can harm consumer interests because there is no suitable competition to encourage lower prices or better-quality offerings. Thus, a monopoly must be regulated and controlled for the common public good.